According to a new report issued by the not-for-profit group Employee Benefit Research Institute (EBRI), many employers were expected to drop workplace health insurance with the introduction of the Affordable Care Act (ACA), and some have done so. However, since 2008 the percentage of employers with 1,000 or more employees offering health benefits to workers has been consistently near or above 99%, reaching 99.8% in 2016. Smaller businesses have shown a steady, though not precipitous, decline in offer rates. For the smallest employers studied, those with fewer than 10 employees, the offer rate declined from 22.7% in 2015 to 21.7% in 2016.

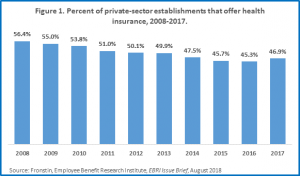

According to the ERBI, by 2017 the overall percentage of private-sector employers offering health benefits increased for the first time since 2008. In 2008, 56.4% of private sector employers offered health benefits. By 2016, it was down to 45.3%. It then increased to 46.9% in 2017. There have been years before 2017 when offer rates increased in various specific establishment size segments, perhaps due to the strengthening economy and lower unemployment rates (Figure 1).

While the overall offer rate trended down until 2017, the percentage of workers eligible for health coverage has been increasing since 2015. Furthermore, the 76.8% of workers eligible for health coverage in 2017 was much higher than the percentage of employers offering such coverage. The juxtaposition between the two trends suggests that workers have been migrating to jobs that offer health coverage. Nearly all large employers offered health coverage before enactment of the ACA and continued to do so through 2017. Over this period, the percentage of employers with 1,000 or more employees that offered coverage was consistently near or above 99% and was 99.3% in 2017.

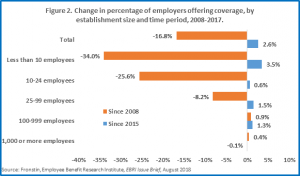

In contrast to large employers, small and mid-sized companies did not stay the course. Regardless of establishment size, the percentage of small and midsized employers offering health benefits started falling as far back as 2009 (Figure 2). More specifically:

Since 2014, the percentage of workers eligible for health insurance in establishments with less than 10 employees has increased from 79.9% to 81.8%. Similarly, the eligibility rate increased from 74% to 76.1% among workers in establishments with 25-99 employees between 2014 and 2017. It increased from 74.8% to 76.6% among workers in establishments with 25-99 employees between 2014 and 2017. It increased from 74.8% to 76.6% among workers in establishments with 1,000 or more workers between 2015 and 2017.

Historically, smaller employers have been less committed to offering health coverage than larger employers. One often-cited reason has been that smaller establishments, more so than larger ones, frequently face higher and more volatile increases in health insurance premiums. Another reason has been that smaller employers are less likely to report linkages between employment-based health coverage and worker attraction and retention. For example, between 68% and 80% of small employers that did not offer health benefits reported no impact on employee recruitment, employee retention, employee attitude and performance, the health of their employees, and absenteeism.

Please contact your Conner Strong & Buckelew account representative toll-free at 1-877-861-3220 with any questions.